")

")

The Invesco CEF Income Composite ETF (PCEF) is an exchange-traded index fund that aims to track the price and yield performance of the S-Network Composite Closed-End Fund Index. As the name of the index suggests, this is an index that consists of closed-end funds that manage assets on behalf of investors in an attempt to obtain money that is used to pay a distribution to investors. As might be expected based on this description, the index will generally have one of the highest yields of any asset available in the American markets. The Invesco CEF Income Composite ETF invests its assets into the securities that comprise this index, so naturally it receives the distributions that they pay out. PCEF then distributes this money to its own investors, after deducting its expenses from the total. As is the case with most Invesco funds, the Invesco CEF Income Composite ETF has a very reasonable expense ratio, so this results in PCEF itself having one of the highest yields that can be obtained from an exchange-traded fund in the American markets. This could make the fund a reasonably attractive investment for an investor who is seeking to earn a high level of income from the assets in their portfolio.

About The Invesco CEF Income Composite ETF

As just stated in the introduction, the Invesco CEF Income Composite ETF is an exchange-traded index fund that aims to track the price and yield performance of the S-Network Composite Closed-End Fund Index. The fund’s website offers the following description:

The Invesco CEF Composite ETF is based on the S-Network Composite Closed-End Fund Index. The Fund will normally invest at least 90% of its total assets in securities of funds included in the Index. The Fund is a “fund-of-funds,” as it invests its assets in the common shares of funds included in the Index rather than in individual securities. The Index currently includes closed-end funds that invest in taxable investment grade fixed-income securities, taxable high yield fixed-income securities and others that utilize an equity option writing (selling) strategy. The Fund and the Index are rebalanced and reconstituted quarterly.

As stated in the description, the Invesco CEF Income Composite ETF is a fund of funds. This is a designation that has long been used in the hedge fund world, but it is much less common to see such a fund trading in the public markets. Investopedia offers a description of a fund of funds:

A fund of funds is one that, instead of investing in a pool of securities like stocks and bonds, buys shares in other funds. These “multi-manager” investments offer investors further diversification and access to the expertise of other skilled fund managers.

In short, the Invesco CEF Income Composite ETF does not invest in common equities, preferred stocks, or bonds like most other exchange-traded funds in the market. Rather, it invests in the common equity shares of closed-end funds that own these assets. As Investopedia points out, this could offer investors a diversification advantage. Rather than purchasing a single closed-end fund and relying on the performance of that fund’s individual manager as a source of investment returns, PCEF provides investors with a way to put their money into many different funds at the same time. The advantage here is that the performance of PCEF should be less affected by the performance of any individual fund manager, and strong performance from a manager who performs well could offset weak performance from a manager who performs poorly during a given period of time. As there is no way to accurately predict ahead of time which managers will do well and which will not during a given period, this proposition may be favorable to an investor who wishes to reduce specific risk (as opposed to systematic risk).

However, there is a downside to the fund of funds structure. This is that the expenses incurred by investors tend to be fairly high. This comes from the fact that each layer of funds has its own expenses. For example, the Invesco CEF Income Composite ETF has a total expense ratio of 2.76%, but not all of this is due to the fees that Invesco imposes on the fund. In fact, PCEF itself only has a management fee of 0.50%. The reason for the 2.76% total expense ratio is that the closed-end funds in which PCEF invests have their own expenses, and as they are typically actively managed funds that employ leverage, these funds have much higher expense ratios than most exchange-traded index funds. For example, these are the largest positions in the portfolio of the Invesco CEF Income Composite ETF as of March 17, 2026:

Invesco

Here are the reported expense ratios for each of these funds, as reported in the funds’ respective fact sheets or websites as of March 18, 2026:

For comparison purposes, the State Street SPDR S&P 500 ETF Trust (SPY), which is one of the largest exchange-traded index funds in the American markets, has a gross expense ratio of 0.0945%. Obviously, that is far below the expense ratios of any of the funds that comprise the ten largest positions in the Invesco CEF Income Composite ETF. As PCEF owns the common equity of the funds in its portfolio, investors in PCEF indirectly incur both the expenses of PCEF itself and the funds that it includes in its portfolio. We can therefore see that the fund of funds strategy provides investors with diversification across fund closed-end fund managers, but it also results in these same investors indirectly incurring fairly high fees relative to other options. The website for the Invesco CEF Income Composite ETF states that the fund’s pro rata share of the expenses incurred by the underlying funds in its portfolio is 2.26%. When combined with PCEF’s own 0.50% management fee, we arrive at a total expense ratio of 2.76% for the fund itself. PCEF currently has a fee waiver and expense reimbursement in place with its adviser until August 31, 2027, which reduces its expense ratio by 0.05%. Thus, as of March 18, 2026, the Invesco CEF Income Composite ETF has a net expense ratio of 2.71%, which is higher than what many investors in exchange-traded funds expect.

The Invesco CEF Income Composite ETF is not an especially large exchange-traded fund, as it only has approximately $784.32 million in assets under management. This is somewhat larger than the Saba Closed-End Funds ETF (CEFS), which is one of the few other exchange-traded funds that invests in closed-end funds. Here are a few other exchange-traded funds that also invest in this asset class and how they compare in terms of size:

(figures are as of March 17, 2026)

As clearly shown, the only one of these exchange-traded funds that is larger than the Invesco CEF Income Composite ETF is the VanEck BDC Income ETF. However, it is questionable whether or not that fund is completely comparable to PCEF. As the name of that fund suggests, the VanEck BDC Income ETF invests its assets in business development companies, rather than the closed-end funds that comprise PCEF’s portfolio. While this is true, we should keep in mind that business development companies are actually just a specialized form of closed-end fund. For example:

- Business Development Companies and Closed-End Funds are both regulated under the U.S. Investment Company Act of 1940.

- Business Development Companies and Closed-End Funds are both closed-ended companies that make their money by actively investing in assets rather than producing a product or service.

- Business Development Companies and Closed-End Funds can both opt to be treated as regulated investment companies for tax purposes.

The difference between closed-end funds mostly has to do with the types of assets in which they invest. A closed-end fund usually invests in publicly traded assets such as common equities, preferred equities, and bonds. A business development company, on the other hand, typically invests in both debt and equity issued by small or mid-sized companies, including privately held companies. The U.S. Securities and Exchange Commission states on its website that business development companies are also legally permitted to use higher levels of debt and leverage than most closed-end funds. In addition to this, business development companies frequently file quarterly financial reports, whereas a typical closed-end fund files such reports semiannually. As such, investors in business development companies may have access to more recent financial information to assist them in making their investment decisions.

The VanEck CEF Muni Income ETF also has some notable differences when compared to PCEF. The most important among these is that XMPT tracks the price and yield performance of the S-Network Municipal Bond Closed-End Fund Index. This is a different index than PCEF tracks, and this particular index only includes those closed-end funds that invest in federal income tax-exempt municipal bonds. The Invesco CEF Income Composite ETF, on the other hand, invests in both investment-grade bond funds and junk bond funds as well as closed-end equity funds that write covered call options against its positions. Thus, PCEF provides exposure to a much wider range of potential assets and funds. This is also evident in the fact that PCEF had 111 holdings on March 16, 2026, compared to 40 for XMPT. However, PCEF will not provide the same level of tax benefits as XMPT, so investors for whom taxation is a major concern may wish to keep that in mind. Anyone who is planning to hold their shares of PCEF in a retirement account will not need to be concerned about this.

The Saba Closed-End Funds ETF is an actively-managed fund that employs an activist strategy to earn profits for investors. That particular exchange-traded fund typically purchases shares of closed-end funds that are trading at a discount to their net asset value. Saba Capital is then known to push on the management of some of the closed-end funds that it holds across its various investment vehicles to make changes that are intended to close the discounts that those funds trade at relative to their net asset values. This is a very different strategy from the passive indexing strategy used by PCEF.

In addition to their size and investment strategies, the four peer exchange-traded funds shown above have very different yields. This chart shows the yields paid by each of these funds as of March 18, 2026:

We can see that the exchange-traded fund that primarily focuses on business development companies has a significantly higher yield than any of the other funds. The fund that only invests in closed-end funds that focus on municipal bonds is the lowest-yielding of the group. This is somewhat unsurprising, as municipal bonds in general tend to have lower yields than most other bonds due to the fact that investors do not need to pay income taxes on the coupons that they receive. This makes municipal bonds rather desirable assets among high-income investors. The other two funds had relatively similar yields as of March 18, 2026.

Many investors generally assume that there is a correlation between an exchange-traded fund’s assets under management and the fund’s liquidity. For example, fund management company AllianceBernstein makes the following statement in an article published on its website:

When an exchange-traded fund is first launched, its lower trading volume and smaller amount of assets under management are often a concern for investors looking to invest sizable amounts.

If we look solely at the average daily volume, we certainly see a correlation between a fund’s assets under management and its average daily volume. This is clearly visible if we look at the Invesco CEF Income Composite ETF and its peers:

(U.S. dollar figures are calculated using the March 18, 2026, closing price for each of the funds)

As we can clearly see, the largest of the funds (BIZD) has a substantially higher average daily volume than any of the other funds. The second-largest of the funds, PCEF, has the second-highest average daily volume, although it is substantially lower than that of BIZD. However, at approximately $2.56 million worth of shares traded per day, the Invesco CEF Income composite ETF should have sufficient liquidity to satisfy the needs of most retail investors. After all, the average retail investor is not purchasing several hundred thousand dollars worth of an exchange-traded fund in a single trade.

In fact, it is unlikely that the average retail investor needs to worry about the liquidity of most exchange-traded funds. As AllianceBernstein points out in the article that I linked right before the table, all exchange-traded funds have contracted with a market maker that is known as an authorized participant. The authorized participant has the ability to purchase shares of the ETF in the market and exchange them for the fund’s underlying assets. It does this whenever the fund’s share price is below its net asset value, and the expectation is that the buying pressure on the fund’s shares will lift the price. The authorized participant also has the ability to do this trade in reverse. It can purchase the underlying assets that make up the fund (known as creation units) and then deliver them to the fund in exchange for shares (the fund creates these shares whenever the assets are delivered). The authorized participant then sells the shares that it received in the market. The selling pressure reduces the ETF’s share price. In effect, the authorized participant is engaging in arbitrage, as it makes money no matter which action it takes, and it assumes virtually no risk to earn this money. Due to the presence of the authorized participant, exchange-traded fund investors do not usually need to worry about the liquidity of a given fund. The only real situation in which liquidity might become an issue is if the underlying assets of the exchange-traded fund are not especially liquid. Closed-end funds, in general, are admittedly not the most liquid assets trading in the public markets, but they should still be liquid enough that retail investors in PCEF should not need to worry about whether or not their individual trade will move the fund’s share price away from the actual value of the fund’s underlying assets. It is, however, possible that a large enough trade could move the price of the underlying assets.

Understanding The S-Network Composite Closed-End Fund Index

As stated earlier, the Invesco CEF Income Composite ETF is an exchange-traded index fund that aims to track the price and yield performance of the S-Network Composite Closed-End Fund Index. As such, we should probably take a few moments to look at this index in order to gain a better understanding of how PCEF may perform in real-world conditions.

The website for the index offers the following description:

The S-Network Composite Closed-End Fund Index is a fund index designed to serve as a benchmark for closed-end funds listed in the US that principally engage in asset management processes seeking to produce taxable annual yield.

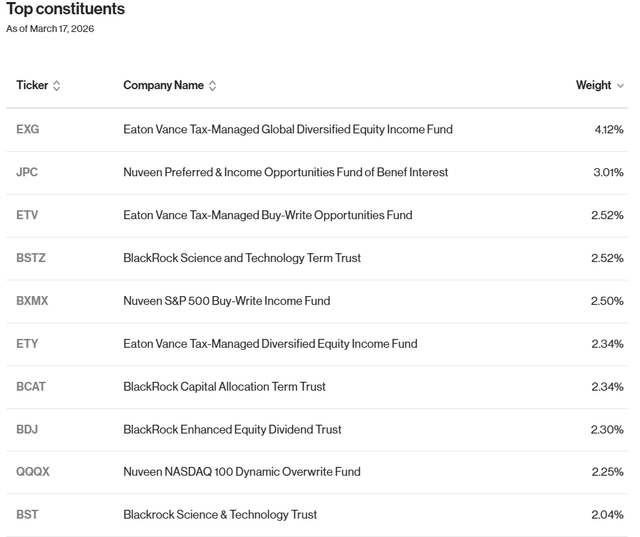

This description clearly states that the index is targeting closed-end funds that aim to provide a high level of current income for their investors. As such, we would expect that the closed-end funds that are included in this index will have relatively high yields, at least when compared to many of the other assets that are available in the American capital markets. This is indeed the case, which we can see by looking at the yields of the top ten constituents of this index. Here they are:

VettaFi

As of March 17, 2026, these closed-end funds were the largest constituents of the index. We can see that most of these names are pretty similar to what PCEF has among its largest holdings. This is expected to be the case due to the simple fact that PCEF is an exchange-traded index fund, and index funds usually achieve their objectives by simply purchasing all of the constituents of an index in relatively equal proportion to what the index possesses. However, we can see that the index has a few slight differences from the fund’s holdings. In particular, the PIMCO Corporate & Income Opportunity Fund was not included among the index’s largest constituents as of March 17, 2026, but it was included among PCEF’s top ten largest positions as of the same date one year earlier. Meanwhile, the BlackRock Science & Technology Trust (BST), which was one of the largest constituents in the index on March 17, 2026, was not included among PCEF’s largest positions as of the same date in 2025. For the most part, though, the Invesco CEF Income Composite ETF has a portfolio that is pretty similar to that of the benchmark index.

Here are the yields of the funds that comprise the ten largest constituents of the S-Network Composite Closed-End Fund Index as of March 18, 2026:

The S-Network Composite Closed-End Fund Index is an index of closed-end funds that primarily focus on providing their investors with a very high level of current income. As we can see from the yields among these funds, it does appear that it is doing exactly that.

We should point out, however, that the S-Network Composite Closed-End Fund Index does not claim to include all closed-end funds in the American equity market, nor does it attempt to do so. The index includes closed-end funds in four specific categories:

- Investment-grade bond funds,

- Junk bond funds,

- Preferred stock funds,

- Equity funds that employ a covered call-writing strategy.

There are several types of closed-end funds that are strictly excluded from this list. For example, the index does not include commodity funds such as the Sprott Physical Gold Trust (PHYS). It does not include common equity funds such as the Adams Diversified Equity Fund (ADX), and it does not include convertible bond funds such as the Advent Convertible and Income Fund (AVK). Thus, the index excludes a number of funds that may be popular among certain investors. However, equity closed-end funds (and convertible closed-end funds) are typically focused on providing investors with capital gains rather than income. While some equity and some convertible bond funds can offer yields that are comparable to the funds shown above, they finance their distributions by realizing capital gains on their assets rather than receiving direct payments in the form of bond coupons or option premiums.

We should also keep in mind that the index is exclusively comprised of closed-end funds that trade natively on a major American exchange (such as the New York Stock Exchange) and are regulated under the Investment Company Act of 1940. There are some foreign companies out there such as RIT Capital Partners (RITPF) or Pershing Square Holdings (PSHZF) that have similar business models to American closed-end funds but do not natively trade on an American exchange. These companies are not eligible for inclusion in the index and thus they are not included in the portfolio of the Invesco CEF Composite ETF.

The methodology document for the S-Network Composite Closed-End Fund Index explains in detail how the fund chooses the specific funds that will comprise the index and how it weights them. In particular, each fund’s assets must consist primarily of the types of securities previously mentioned and meet the following criteria:

- The fund must have at least $75 million in assets under management,

- The fund’s share price must be within 25% of its net asset value for ten days prior to the rebalancing date,

- The fund’s management fee must be below 1.50%,

- The fund needs to have an average daily volume (measured in U.S. dollars) of at least $500,000,

- The fund must have been trading in the market for three months,

- Term funds must not have a termination date within the next three years.

These rules appear to be designed so that the index will exclude any very tightly held funds or funds for which liquidity may be an issue. As was already mentioned, exchange-traded funds can sometimes run into liquidity problems if the underlying assets are not especially liquid, so indices that are designed to be tracked by an exchange-traded fund usually have rules in place to ensure that the fund’s assets are mostly liquid ones.

The S-Network Composite Closed-End Fund Index employs a weighted net asset value system to determine the proportional weight of each fund that is included in the index. Thus, for the most part, the higher a fund’s net assets, the higher its weight in the index. However, the weight of any individual closed-end fund is capped at 8%. If any individual fund has a sufficiently large net asset value to otherwise be 8% of the index, then anything over 8% is proportionally distributed among the other funds that comprise the index. In addition to this rule, the index also has a rule that states that the total weight of all funds that would otherwise represent more than 5% of the index shall be capped at 45% of the total weighting. This rule prevents a handful of funds from accounting for more than half of the index. It also works pretty well with the U.S. government’s regulation that forbids a regulated investment company from having its assets disproportionately allocated to only a handful of securities. Under Federal regulations, the total weighting of all securities accounting for more than 5% of an RIC’s portfolio cannot be above 50%. Due to this rule, many indices that are designed to be tracked by an index fund limit the weightings of the most heavily weighted securities in the portfolio to comply with this regulation. The S-Network Composite Closed-End Fund Index is included among this group. As was the case with the 8% rule, if the index has a few sufficiently large positions to be in violation of this rule, then any amount in excess of 45% is distributed among the smaller funds in the index. Finally, those closed-end funds that typically trade with a large discount to net asset value receive a slight increase in their weighting in the index and those closed-end funds that typically trade at a large premium to their net asset values receive a slight decrease in their weightings in the index.

The S-Network Composite Closed-End Fund Index is rebalanced and reconstituted on the last business day of each calendar quarter (in the months of March, June, September, and December). Presumably, the Invesco CEF Income Composite ETF adjusts its own portfolio on the first available opportunity after the index rebalancing.

Understanding Closed-End Funds

There are a few different types of investment funds in the market, and closed-end funds are the least common. The portfolio of the Invesco CEF Income Composite ETF only invests in closed-end funds, though, so investors in the ETF should understand how they work.

A closed-end fund is somewhat similar to an exchange-traded fund in that both types of funds trade on a stock exchange, such as the New York Stock Exchange. The difference, however, comes from the fact that a closed-end fund has a fixed number of shares outstanding.

Earlier in this article, I explained how the authorized participant works to keep the share price of an exchange-traded fund in line with the value of its underlying assets. The arbitrage that the authorized participant engages in causes the number of shares outstanding of the fund to increase or decrease with investor demand and the fund’s net asset value. This is not the case for a closed-end fund. Rather, a closed-end fund issues a specific number of shares in a single issuance (this could be at the time that the fund is first established or through a regular share offering). The fund manager of the closed-end fund then invests the fund’s assets in accordance with the fund’s prospectus and objectives. The share price of a closed-end fund is determined by other market participants. As is technically the case with the common equity of a corporation, the share price of a closed-end fund simply depends on what another market participant will pay for it at any given time. This can, on occasion, result in a given fund’s share price being quite different from the actual value of its underlying assets. The share price of a closed-end fund thus does not necessarily go up whenever the fund’s portfolio gets larger due to capital gains. The fund’s share price also does not necessarily go down whenever the fund’s portfolio suffers losses.

Closed-end funds also pay out most or all of their net investment income and net realized capital gains to their investors. This usually results in these securities having some of the highest yields that are available in the market. While an exchange-traded fund technically has to do the same thing (as ETFs are usually regulated investment companies just like closed-end funds), many exchange-traded index funds rarely realize capital gains and so do not have any realized gains to pay out. Closed-end funds, on the other hand, are almost always actively managed funds that frequently realize their gains.

Tax Considerations

As already mentioned, the closed-end funds in the portfolio of the Invesco CEF Income Composite ETF consist primarily of funds that invest primarily in fixed-income securities and covered call-writing funds. This could make PCEF somewhat problematic for investors who are in a high federal income tax bracket and are investing using a taxable account.

One of the characteristics of a regulated investment company is that they act as a pass-through entity for tax purposes. This means that the company itself does not pay corporate taxes. However, its distributions are then taxed as if the fund’s investors held the assets directly. This can be problematic for bond funds because coupon payments made by a bond are taxed at the ordinary income tax rate, rather than at favorable capital gains rates. The distributions that PCEF receives from the closed-end bond funds in its portfolio may therefore be considered ordinary income, depending on whether the money came from bond coupons, capital gains, or return of capital. When it distributes this money out to its own investors, those investors will therefore have to pay ordinary income taxes on these distributions. Ultimately, this means that investors in PCEF may have higher tax liability than they would if the fund paid out the same distribution yield but the money came from long-term realized capital gains.

Financial advisors typically recommend holding any funds that derive a significant proportion of their income from bonds in a retirement account or some other form of tax-advantaged account. While this fund’s income is not entirely from bonds (and thus the tax liability should be lower than it would be for a bond fund with the same yield), investors in high tax brackets might still want to consider using a retirement account to purchase the shares rather than an ordinary brokerage account.

Conclusion

In conclusion, the Invesco CEF Income Composite ETF is an exchange-traded index fund that tracks the price and yield performance of the S-Network Composite Closed-End Fund Index. This is an index that is comprised of income-focused closed-end funds investing in bonds, preferred stocks, and covered call-writing strategies. The index specifically excludes equity and convertible bond funds, and it also excludes funds that do not have American listings. The fund will generally have a higher yield than many other ETFs, but some of its distributions will be taxed as ordinary income, and thus it might be advisable to hold its shares in a tax-advantaged account.

This article answers these three main questions about PCEF:

- Why is the expense ratio for PCEF so high?

- Is PCEF better suited for a regular investment account or a tax-advantaged account?

- How are the holdings of PCEF chosen?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Presents at BofA Securities 2026 Information & Business Services Conference Transcript")

")